- Dollar Debrief

- Posts

- What is the Difference Between Credit Card Issuers and Networks?

What is the Difference Between Credit Card Issuers and Networks?

And Should I Even Use a Credit Card?

Mike Moricz

July 18, 2024

Credit cards are a HOT topic in the realm of personal finance. Despite your feelings on credit cards, knowing how they work can be useful. If nothing else, educating people on the difference between credit card issuers and networks can make for some REALLY cool small talk at parties.

What is the difference between credit card issuers and networks?

There is a lot that happens behind the scenes every time you swipe your credit card for gas station sushi or for your 27th Prime Day purchase (because you’re fiscally responsible and actually SAVED money by dumping loads of money on Prime Day).

There are two major parties involved in credit cards, known as credit card networks and credit card issuers.

If you look at your credit card, you’ll probably notice a couple of different logos/companies listed on there.

Somewhere on the front of your card, you’ll likely see the financial institution you applied for the card through, like Chase, Capital One, Citi, or Bank of America. These institutions are known as the credit card issuers, since, well… they issue you the credit card.

Credit card issuers manage various features of credit cards, such as the card application/approval process, deciding on the terms and benefits of the card, collecting payments from cardholders, and more.

They also decide what your credit limit will be based on your credit score, history, and debt-to-income ratio.

Somewhere else on your credit card, you’ll probably also see Visa, Mastercard, American Express or Discover displayed proudly. These represent the four major credit card networks, whose purpose is to facilitate transactions between merchants and card issuers.

Card networks create virtual payment infrastructures and charge merchants fees for processing credit/debit card transactions. Networks are the middlemen between merchants and credit card issuers.

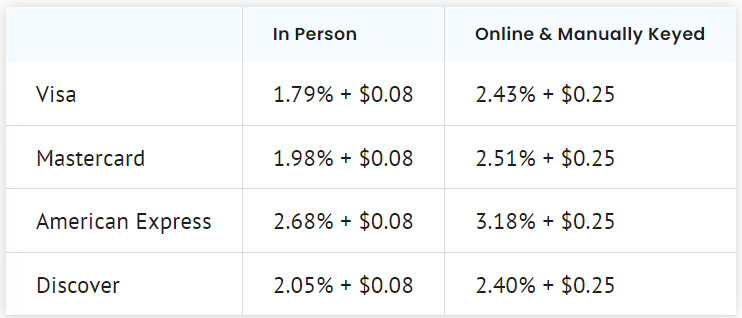

Card networks also determine where your credit cards are accepted. Not every merchant accepts every type of card network, because each network charges the merchant a different fee for using their services. These fees vary depending on the size of the purchase and whether the purchase is in person or online.

Average credit card fees per major network (Source: Motley Fool)

Visa and Mastercard, with a longer history and generally lower average fees, are accepted by virtually every merchant both in the US and internationally.

Discover and American Express are still working to catch up. Although they both reportedly have reached a 99% acceptance rate among US merchants, they are still VASTLY under-represented by merchants overseas.

If a merchant doesn’t like the fee structure of a certain network and the juice isn’t worth the squeeze for them, they can happily decline to accept that network.

If you’ve ever faced the public rejection of being denied usage of your American Express Platinum Card®, you’ll know what I’m talking about.

Although consumers don’t directly pay this fee to the network (merchants do), the increased cost for the merchant is often just rolled over to the customer through an increased price in goods or services, because everyone’s just trying to get theirs.

Two of the four major card networks (AmEx and Discover) are both card networks and card issuers, so they play by the rules they set.

Card networks also offer purchase protections and have partnerships across numerous industries like dining, travel, and transportation to incentivize card issuers to use their service, so they can make more money.

Here’s an example of how credit card transactions pan out behind the scenes, using my beloved Chase Sapphire Reserve Card®, which runs on Visa’s network.

I swipe my card at Publix for a chicken tender Pub sub (the supreme grocery store in the US)

Publix sends the transaction to Visa

Visa sends the transaction to Chase

Chase reviews and approves/denies the transaction, then sends the decision back to Visa

Visa sends the decision along to Publix and the transaction is approved or denied.

I eat my sub

All of this happens more or less instantaneously, which is kind of insane if you think about it. All fraud decisions by the card issuer are made in the couple of seconds it takes the card scanner to process the transaction.

So, what’s the point of all this?

Well, knowing where you plan on using your card (stateside versus overseas), understanding merchant preferences, and comparing various card rewards offers can help you make an informed decision of what credit card is best for you.

If you decide to open a credit card (which we recommend for building your credit score which, despite what some say, is actually pretty important for things like buying a home with a favorable interest rate), the following principles will help you stay out of perpetual credit card debt:

Use your credit card like a debit card. Only swipe on purchases that you have enough money in your checking account to cover.

Pay off your credit card in full each month. This prevents you from accruing interest on your credit card and keeps your debt-to-income ratio low, further boosting your credit score.

Don’t be a dummy.

Together, credit card networks and issuers work together to achieve three primary goals: 1) make money, 2) help you spend money easier, and 3) spite Dave Ramsey.

What We’re Reading/Listening To:

Designing Your Life by Bill Burnett and Dave Evans. I’ll be starting school again in a few weeks and reading this book is one of the entrance requirements for the program. Turns out I’m not much better at school now than I was when I graduated college, as I’ve procrastinated on opening the book until yesterday.

Since I’m only in the introduction chapter, I’ll use their words to describe it. This book is supposed to show us “how design thinking can help us create a life that is both meaningful and fulfilling, regardless of who or where we are, what we do or have done for a living, or how young or old we are.” Sounds neat.

Debrief on Deck

Next week, Wilson will dive into how charitable donations work, what tax benefits you can get from them, and how to give charitably in a tax savvy way.

Because why else would anyone want to donate to a good cause other than for the tax bennies?

(I’m kidding, don’t cancel me)

As always, please reach out to us with any questions or comments you have. You can reply directly to this email or find us on social media (X (formerly Twitter) and Instagram).

Until then, stay the course.

Mike