- Dollar Debrief

- Posts

- Flashback for 50 Newsletters

Two dudes. One mission. 20(?) toes. 34 Yankee Candle references (soon to be 35). Countless low quality homemade memes and dad jokes. 50 NEWSLETTERS. What a ride it has been.

Flashback for 50 Newsletters

It’s crazy how life works. One day, two dudes and their wives go out to eat BBQ together and one (Wilson) proposes the idea of a finance newsletter. The next day, we’re 50 newsletters deep and counting.

If you’re new here or if you’re an OG (shoutout to Todd Meyer the 🐐), here’s a reminder that you can access any of our previous newsletters by going directly to our website. For this letter, we wanted to reflect on ten highlights over the past 50 newsletters. For those who sucked at school like me, this is the SparkNotes version of a lot of what we’ve written.

1. How Can I Retire Early? (Letter #3)

Let’s start from the top. I’m always an advocate for figuring out what you want out of life before trying to decide what to do with your money.

This picture gives off strong old-school dad comic energy

In case you didn’t know, you don’t have to wait until your 60s or 70s to retire. We think that work is important and that contributing to society is a good thing. But there’s a better way to do it than grinding for 40 years in a job you hate.

If you don’t want to work until you die, you’ll need to build passive income streams (money that requires little to no effort to earn and maintain) to cover your living expenses in retirement. If you plan to spend $5,000 a month in retirement, you’ll need to build an investment portfolio of some combination of stocks, bonds, real estate, businesses, or other income-generating things to produce at least $5,000 monthly.

Once your passive income grows to the point where it covers your expenses, you’ve reached financial independence. You can then make life and work decisions without financial constraints being the main deciding factor. And that’s a pretty legit situation to be in.

Fun fact: this was our most read letter with an 85.1% open rate.

2. How Much Money Do I Need to Retire? (Letter #10)

Your ability to retire isn’t decided by an age, but a dollar value.

For those who choose the route of stock market investing, you’ll need to have somewhere between 25 and 33.3 times your estimated annual retirement expenses (not your current expenses) invested to retire. In other terms, if you can live off 4% or less of your total investment portfolio each year, you can retire with a solid chance that you won’t run out of money.

Your retirement length and investment choices obviously influence your chance of success. Check out the letter to see how different stock/bonds combinations and different withdrawal rates have performed in the past and to determine your own FI number.

3. How Do I Invest in the Stock Market? (Letter #4)

So you decided you want to give this financial independence thing a go and that you want to invest in the stock market.

Sounds great… but how? It’s easier than you think.

Pick a brokerage (Fidelity, Schwab, and Vanguard are our three favorites), open an account (like a brokerage account or IRA), link your checking account, transfer money from your checking account to your investment account, and then invest that money in stocks, bonds, ETF, mutual funds, etc.

Stock market investing is as easy as shopping on Amazon on Prime Day, especially if you understand what to invest in.

4. Should I Use a Financial Advisor? (Letter #19)

“Investing sounds annoying. Shouldn’t I just pay for someone to do it for me?”

If you enjoy underperformance, high fees, and used car salesmen, then have at it. If you aren’t a glutton for punishment, then probably not.

But should you pay a fiduciary financial advisor a one-time fee to review your financial plan and cover any blind spots you have? Maybe. Check out the letter to decide for yourself.

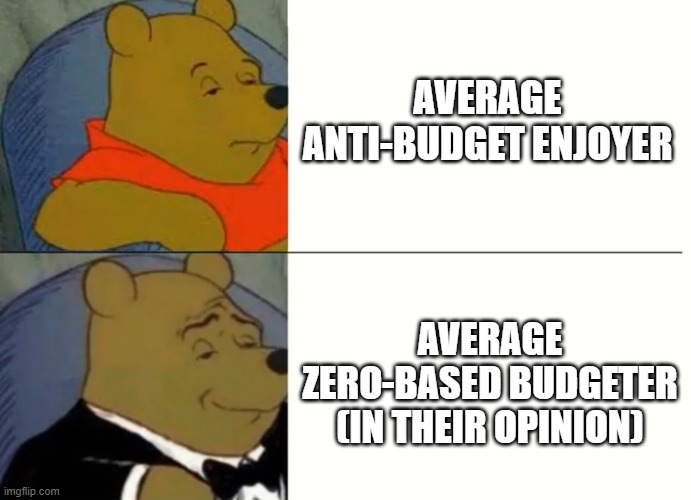

5. Zero-Based Budget vs. Anti Budget - Which is Better? (Letter #12 and Letter #42)

It’s hard to control your money if you don’t have a plan for it. Budgeting is simply creating a plan for your money.

The two budget styles we like are zero-based budgets and anti-budgets. Two very different styles for different people.

Zero-based budgets give you maximum control over your money, where you create a plan for every dollar you earn and track every expense you make to reach your savings goals. The downside is that zero-based budgets require a good amount of effort to keep up with.

Anti-budgets are a less intensive way to budget, putting your savings aside first and then spending freely for the rest of the month, ensuring you don’t run out of money. This is a MUCH easier way to budget and save, but you don’t have nearly as much control over your money.

Which one is better? The one you can stick to and that works for you. I’m (Mike) a zero-based budget guy and Wilson is team anti-budget. But guess what–we’re both billionaires (plus or minus a few bucks).

6. How Do I Work Out of Debt? (Letter #5)

The debt avalanche is the best way to pay off debt.

The process is simple. Continue making minimum payments on all of your debts. Throw all of your available money toward your debt with the highest interest rate first. Once that first debt is paid off, throw all available money including the minimum payment of the paid off debt at your second-highest interest rate until it’s gone. Continue this process until you’re debt free.

7. What is Good Debt? (Letter #9)

Some see all debt as bad. We see debt you take on for liabilities (like cars and credit card debt) as something to avoid, but debt taken on for assets (things that appreciate in value or positively cash flow like a rental property) can be a tool to help you build wealth.

Disclaimer: many people have found themselves bankrupt for poorly managed “good” debt (even Dave Ramsey). Don’t bite off more than you can chew.

8. Should I Buy a House? Parts 1-3 (Letter #13, Letter #15, Letter #24)

Buy or rent is the million-dollar question. The answer is that there is no answer. The decision to buy or rent is a highly personal one.

Wilson’s three-part series dove into the costs of homeownership (spoiler, there are a lot), home appreciation, inflating rents, fixed mortgages, and ways to extract additional value from a home you own.

Skim through this series to inform your decision.

9. November Monthly Market Debrief (Letter #34)

Sometime in November, Wilson was meditating amid 80 Yankee Candles when he had an epiphany.

“What if we sent a monthly letter reviewing the market’s performance and notable finance happenings?” Hence, the monthly market debrief was born.

Since then, we’ve covered OpenAI’s game of thrones, Apple and Masimo’s David and Goliath-esque legal showdown, Stanley cups (the drinking ones, not the cool hockey one), moon landings (if you believe the moon is real), and more.

10. How Soon Can I Retire? (Letter #41)

Well, that’s entirely up to you. Your savings rate is the primary determinant of how soon you can retire.

Are you comfortable working for 66 years? Save just 5% of your income and you’re good to go. Want to retire in 3 years? Better find a way to save 90% of your income.

The realization that your financial future is 95% in your hands can be either intimidating or empowering, depending on your point of view. Take ownership of your finances and make mostly smart money decisions, and you’ll be well ahead of those who do neither.

We have a lot of good content lined up over the coming months, including evaluating more investment options (like gold), whether the military pension is worth the grind, killer personal finance apps and tools we love, and MUCH more.

We’re endlessly thankful for you all who decided to join the circus and let us bless your inbox once a week with our money ramblings.

Our purpose for this newsletter remains the same–to help people take control of their finances and build a dope, financially stable life. We hope we’ve helped you progress toward this goal.

Debrief on Deck

Next week is our Monthly Market Debrief for March! The Fed said WHAT about interest rates?? Tune in next week to find out.

As always, please reach out to us with any questions or comments you have. You can reply directly to this email or find us on social media (X (formerly Twitter) and Instagram).

Until then, stay the course.

Mike