- Dollar Debrief

- Posts

- Is the Military Pension Worth It?

Ignoring the downsides of military service (most notably the bird-sized mosquitoes at Fort Johnson, LA), military service has its perks. But the best perk isn’t the pension or free healthcare, it’s the waived annual membership fees for fancy credit cards that give you access to airport lounges. I’m writing this from the lovely Delta Sky Club in Raleigh while crushing some hashbrowns and coffee. No need to thank a Soldier for their service, just keep up the airport lounge access.

Is the military pension worth it?

It depends on which of the two retirement plans you fall under, your life goals, your general happiness and career satisfaction in the military, your financial preparedness if you didn’t have the safety blanket of a military pension, and a number of other considerations.

Service members are eligible for a pension after 20 years of service. If you’re active duty, your pension kicks in right when you exit the military. If you're in the national guard or reserve, it kicks in at age 60, or even earlier if you’ve accumulated some active duty time or you stay in for more than 20 years.

Let’s break each deciding factor down one at a time, starting with the most important.

Your general happiness and career satisfaction

If you’re miserable in the Air Force, Navy, or Space Force (or even Coast Guard, if you consider that the military), grow your pain tolerance and get over it by comparing your quality of life to your Army or Marine brethren.

Depiction of the hardest day in the Navy

Kidding, kidding.

If you’re miserable in the military, it’s best to get out. If you’re unsatisfied with your career in the military, evaluate your options for a career change within the military and if those don’t suit your fancy, get out.

Serving half-heartedly in the military has much greater consequences than in any other career. You never know when you’re going to be called to deploy, and if you do, you’re going to want to be surrounded by people who are bought in and committed to the cause.

Now, if you’re over the 10-year hump and you can see the light at the end of the tunnel, you’ll have to do a cost-benefit analysis.

If you don’t enjoy what you’re doing with your career, is the pension worth grinding it out until 20 years? This is both a personal and a financial decision, but I recommend weighing the personal side more heavily.

Is continued service and the stressors that come along with it going to cost you your marriage, your relationship with your children, or any other non-negotiables for you? Get out and don’t look back. If not and if you’re enjoying what you’re doing, stay in until retirement.

If you decide you want out, make sure you’re not just running from the military, but instead running toward something meaningful to you on the outside. And that you have a plan to secure your own retirement without the comfort of a pension.

Let’s look at what you’re missing out on if you do decide to get out.

The total value of military retirement

Military service members fall under one of two retirement plans: High-36 (legacy plan) or the Blended Retirement System (new plan).

The High-36 plan takes your base pay average from your highest-earning 36 months of service (so probably your last three years unless you get demoted) and multiplies that dollar value times your number of years of service, then times 2.5%. So it’s:

Highest 36-month base pay average x Years of service x 2.5%

Someone whose highest base pay average is $6,000 who served 20 years will earn $3,000 a month every month in retirement pay. To get 100% of your base pay under the High-36 plan, you’d have to serve 40 years (gross).

The biggest difference with the Blended Retirement System is that you multiply your base pay average and years of service by 2% instead of 2.5%, reducing your pension. In exchange, the military matches your TSP contributions up to 5% while you’re still in, making it a better option for those who aren’t planning to retire in the military since you’ll at least walk away from the military with something.

The same guy whose base pay averaged $6,000 a month would earn $2,400 a month instead of $3,000.

However, military retirement benefits include more than just a pension.

Military retirees also get TRICARE health insurance for life, both for themselves, their spouses, and any children under 21. This warrants a whole other letter by itself, but in the words of my wife: “TRICARE be good.”

Since all disabled veterans (not just retirees) are eligible for VA disability pay as compensation for ailments suffered as a result of military service, I won’t count this as a benefit unique to retirees.

Your financial preparedness without a military pension

If you are unwilling to invest toward your own retirement, stick around for the military pension.

If you are willing to invest toward retirement, you’ll want to do another cost-benefit analysis to see how much money you’d leave on the table if you decided to leave the military before you’re eligible for a pension.

Let’s total the value of military retirement.

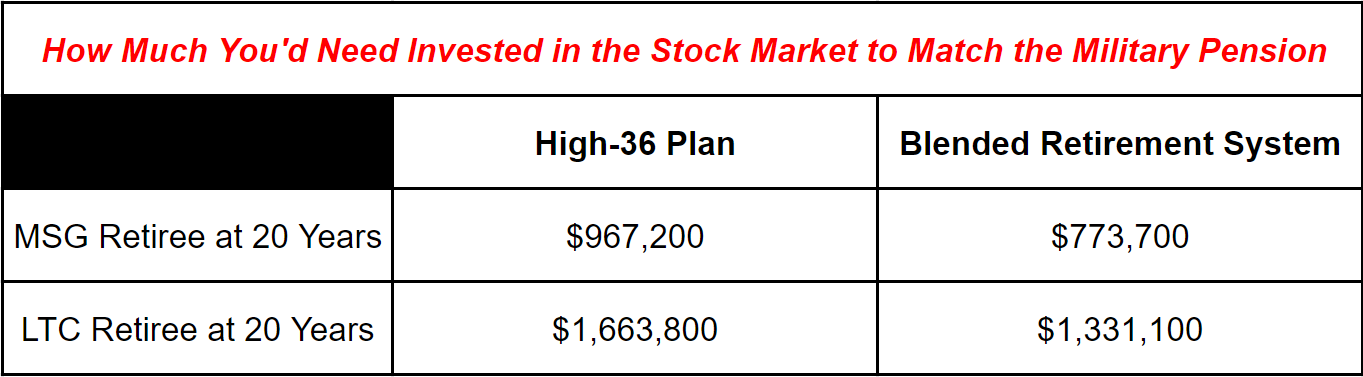

In 2024, a Lieutenant Colonel (LTC) with 20 years of military service earns $11,093 in base pay while on Active Duty. A Master Sergeant (MSG) with 20 years of service earns $6,449.

Under the High-36 plan, these numbers translate into $5,546 in pension money per month for the retired LTC or $3,224 a month for the retired MSG.

These numbers drop to $4,437 (LTC) and $2,579 (MSG) for those under the Blended Retirement System.

Let’s see how much you’d need to have invested in the stock market to earn an equivalent passive monthly income to a military pension (assuming a 4% withdrawal rate):

That’s a hefty amount of money. To build a nest egg that rivals that of an LTC retiree under the High-36 plan, you’d have to invest roughly $3,030 a month, every month, for 20 years.

Maybe that’s possible for you based on your current monthly income, maybe it isn’t.

The decision to stay versus go is a tough one, but my overall recommendation is to look at the personal aspect of the decision first, then the financial one.

But fret not, I’ve boiled the decision down to another highly technical quad chart to help guide you.

I’m accepting commissions for custom graph and chart drawings

Military retirement can be a cheat code for early retirement, but it’s not the only path to making it happen.

Call to Action

If you’re in the military and aren’t sure if you want to stay in or get out, use this letter to help inform your decision!

What We’re Reading/Listening To:

I’m not sure if this qualifies him as a genius, but my two-year-old can spit The Itsy Bitsy Spider from memory in broken English. And boy, does he love showing off his newfound talents.

Debrief on Deck

Next week is our Monthly Market Debrief for April! Is the interest rate situation looking bleak after all? Will we get a Yankee Candle reference after a long drought without one? Tune in next week to find out.

As always, please reach out to us with any questions or comments you have. You can reply directly to this email or find us on social media (X (formerly Twitter) and Instagram).

Until then, stay the course.

Mike