- Dollar Debrief

- Posts

- How Much Money Should I Invest Each Month?

Why does the question “how much money should I invest each month” elicit responses that sound like a river troll is demanding you solve a riddle before you can cross the bridge?

How much money should I invest each month?

Is it just me, or is the blanket answer to this question always somewhere between 10% or 20% of your take-home pay, regardless of your financial situation or goals?

Dave Ramsey advocates saving 15% of your take-home pay, followers of the 50/30/20 rule preach 20%, and your grandma says to throw 10% in a whole life insurance policy because “iT’s A gReAt InVeStMenT.”

Don’t take investment advice from your grandma, unless she’s telling you to buy index funds

However, this advice is dumb. Blanket statement financial advice about something as personal as retirement savings is rarely helpful.

Instead of throwing out nebulous percentages and rules of thumb out there, let’s look at hard numbers based in reality and on YOUR personal financial situation.

This newsletter is going to read more like a handbook than a newsletter. It took me less time to write and you won’t have to hear me flap my gums for as long. It’s a win-win.

Here’s the process to determine how much money you need to invest each month.

Step 1: Decide when you want to retire

For starters, you need an idea of when you want to retire.

If you want to retire at 40, good on you. Don’t let pessimism deter you from picking the age you actually want to retire. That’s a problem for two-minutes-from-now you.

The next steps will help you determine if your retirement target is realistic based on your current and projected savings habits.

Step 2: Determine how much money you need to retire

Next, you need to figure out your FI number. This is the amount of money you need to have invested in order to retire. You can’t know how much money to save each month if you don’t know how much money you need.

Am I starting to sound like a river troll? If so, start here for help with deciding your FI number before moving onto the next step.

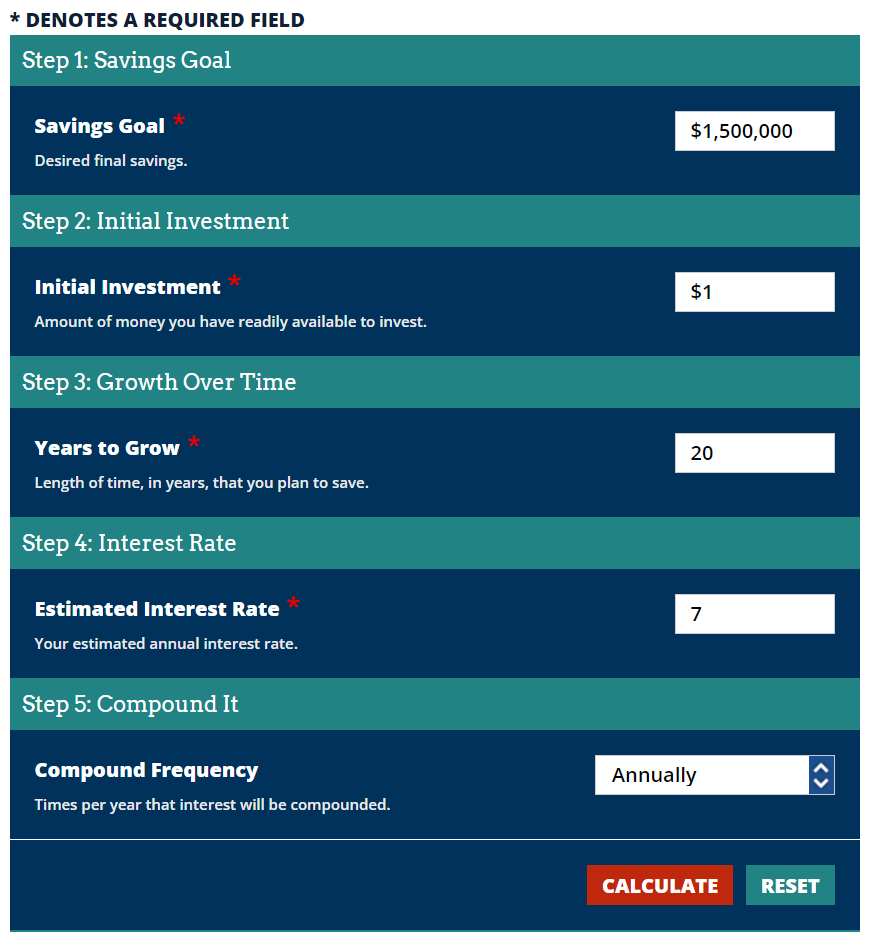

Step 3: Hop on Investor.gov’s Savings Goal Calculator and run the numbers

Investor.gov may truly be the only government-designed website that isn’t trash. There are all kinds of fun (for me) calculators to help you shape your financial goals.

Click this to access the Savings Goal Calculator. It’ll look like this:

Next, you just fill out the calculator:

Savings Goal: Input your FI Number

Initial Investment: Input however much money you currently have invested (not in a savings account). If you have no money invested or set aside to invest, put “1” (since the calculator won’t let you put 0. If you have no money invested but you have some money set aside to start investing, use that dollar amount.

Years to Grow: Input however many years are between your current age and the age you want to retire. If you’re 30 and want to retire at 50, type in “20.”

Estimated Interest Rate: The historical annualized S&P 500 return since inception has been roughly 10%. Input 10% if you don’t want to consider inflation when running the numbers, or 7% if you do. This assumes you’re invested 100% in US index funds/ETFs. If you’re invested in bonds, drop this percentage accordingly

Compound Frequency: Keep this at “Annually”

Once complete, hit calculate.

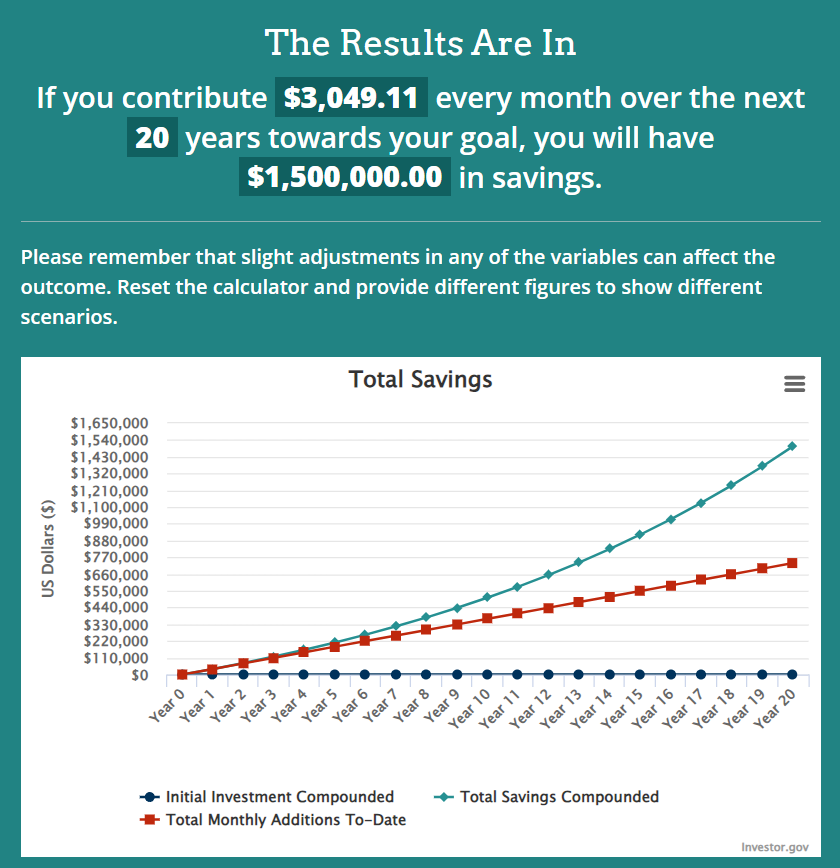

Here’s how you would fare as someone wanting to retire in 20 years with $1.5 million invested:

Boom, we went from a nebulous investment percentage to a hard dollar value to base your monthly retirement savings on.

Step 4: Confirm or adjust your retirement plan based on the resulting monthly savings amount

The number you’re left with may be bigger or smaller than you expected. If you’re this guy^, is investing $3,049 a month more than you can currently swing?

If so, you have three options: a) push your retirement age later, b) make your FI number smaller (if you are able and willing to reduce your retirement spending), or c) figure out a way to earn more and/or spend less now to free up enough money to meet your savings goal.

Retirement planning doesn’t have to feel like shaking a magic 8-ball and hoping you have enough money saved when you want to retire. With a little bit of planning, you can successfully solve the river troll’s riddle and continue your journey across the bridge and toward financial independence.

Call to Action

Crunch the numbers for yourself based on your target retirement age and FI number! See if you’re on track to meet your retirement goals and if not, evaluate what changes you can make to get there.

What We’re Reading/Listening To:

Podcast: Two Sides of FI. The hosts, Eric and Jason, are two buddies on opposite sides of financial independence. One is a retiree and one is on his way there. Give it a listen if you’re interested in financial psychology, early retirement, and personal stories of those who made FI happen.

Debrief on Deck

Next week, we’ll be answering any and all questions you send in! Have a question (finance related or not) that you’re afraid to ask your friends and can’t find a good answer to online? Give us a shot and send it our way by replying to this email or sending it via social media.

As always, please reach out to us with any questions or comments you have. You can reply directly to this email or find us on social media (X (formerly Twitter) and Instagram).

Until then, stay the course.

Mike