- Dollar Debrief

- Posts

- What is a Rising Equities Portfolio?

No, Rising Equities Portfolio isn’t the 153rd installment of the Star Wars series. Yes, it’s a way to protect your hard earned money from stock market crashes early in retirement.

What is a rising equities portfolio?

Hypothesize with me for a minute.

It’s February 2020 and you’re finally ready to retire from your 40-year career at the bank. Your retirement savings are looking healthy, you’ve reached your FI number, and you’re confident in your retirement plan with a 100% stock allocation. Bonds are for nerds anyway, right?

You flip off your boss on the way out of work for the last time and you’re finally free… until a little virus known as COVID-19 rocks the US stock market on February 20th, 2020.

Without a cash buffer to cover your expenses until the market recovered, you’re forced to withdraw from your portfolio at a 34% loss, eating significantly into your retirement savings. Your portfolio never recovers from the early blow it took. You decide it’s time to give your old career another try, apologize to your boss for flipping him off, and get back to work.

A bit dramatic, I know, but what I just described is an investment problem called sequence of returns risk. Sequence of returns risk can kill a stock-heavy investment portfolio faster than South Dakota Governor Kristi Noem kills her dogs.

This risk describes the order in which your investment returns occur. Market downturns early in retirement and later market gains are much worse for a retiree than early market gains and later market downturns, with all other factors being equal. Poor market performance early in retirement can shrink your portfolio to the point where future market upswings aren’t enough for it to recover. This increases the risk that you'll run out of money.

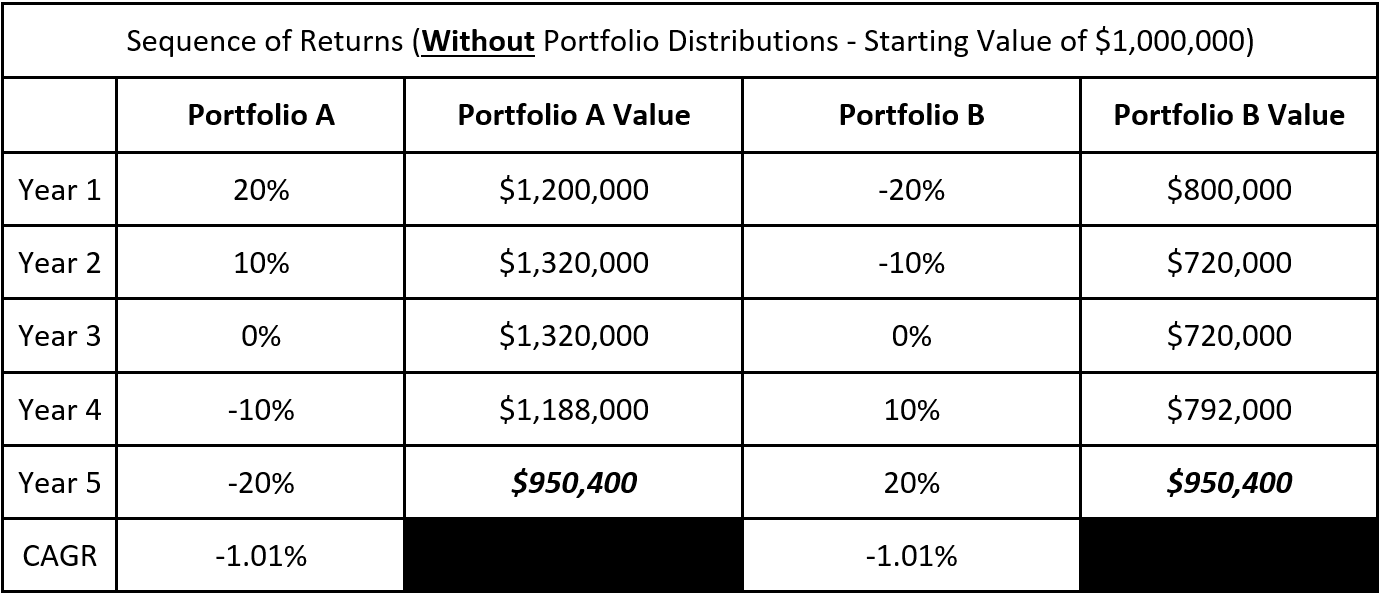

Let's see how this plays out in practice. Below are two portfolios with an identical starting value ($1 million) and compound annual growth rate (CAGR, AKA annualized return), but different sequences of returns. This first chart shows what this looks like if you aren’t withdrawing any money from your investments.

As you can see, sequence of returns risk isn’t a big deal if you aren’t withdrawing money from your portfolio. It’ll be a rough five-year period to be an investor, but you’ll probably eventually recover either way the returns happen if you’re in it for the long haul. It’s when you start pulling money out when the problems start.

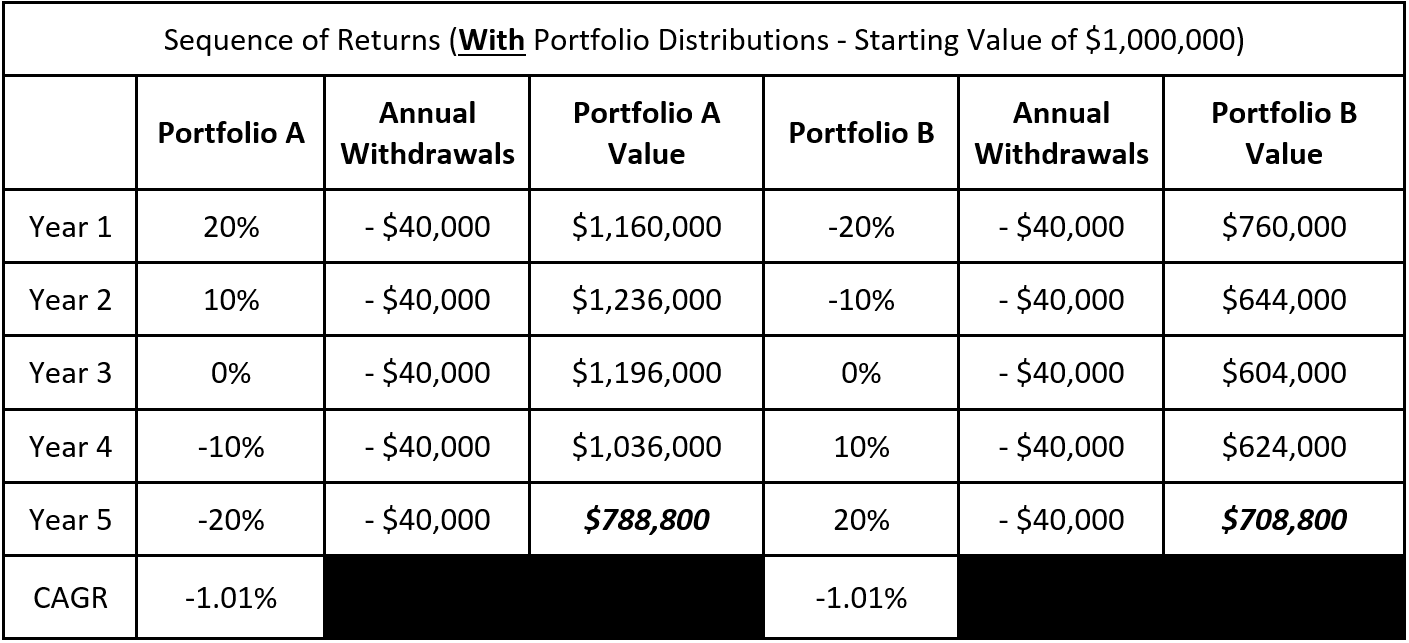

Let's look at the same two portfolios, but this time, including $40,000 (4%) distributions each year to cover living expenses.

Portfolio A lost 21% of its initial value in five years, while Portfolio B lost 29% of its value since it suffered greater market losses upfront. In only five years, Portfolio B holds $80,000 less than Portfolio A, which is equivalent to two years' worth of this person’s living expenses.

PSA: Stocks and equities are the same thing. I’ll use both interchangeably in this letter, and I wanted to give you fair warning to prevent confusion.

Get to the point, Mike.

Alright, alright. So what does a rising equities portfolio have to do with any of this?

Well, it’s arguably the best way to fend off sequence of returns risk, although it contradicts most traditional asset allocation advice.

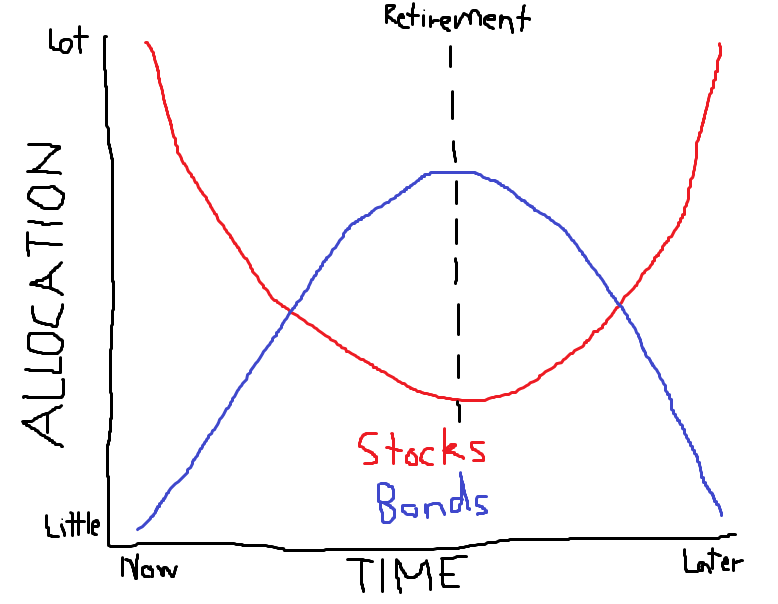

Traditional financial planning for retirees has long favored a decreasing equities portfolio, where you decrease your stock allocation and increase your bond allocation as you age. Similar to this chart that I showed in our target date funds letter.

Seems logical, right? The older you are, the less risk and volatility from stocks you want to take on. It briefs well, but there might be a better way to plan your retirement asset allocation.

They say that plagiarism is the purest form of flattery. I’m about to flatter the heck out of some research done by two dudes way smarter than me.

Retirement researchers Wade Pfau and Michael Kitces have challenged traditional retirement portfolio planning by advocating for a rising equities portfolio. This is where you decrease your stock allocation until retirement, and then slowly increase it over time to capture more stock market gains later in retirement when sequence of returns risk is less of an issue. This strategy “starts out conservative and becomes more aggressive through the retirement time horizon.”

On a graph, it replicates a U-shaped equities allocation, where the bottom of the "U" marks the start of retirement.

But why would you do this? They concluded that this strategy can potentially “reduce both the probability of failure and the magnitude of failure” for retirees.

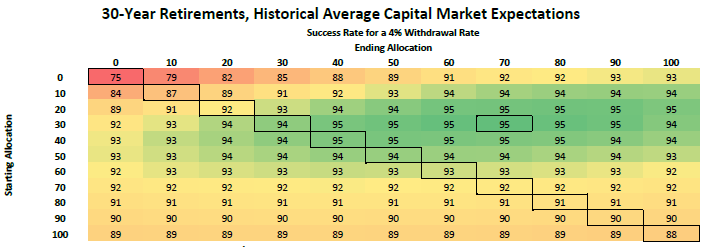

Using historical market data, Pfau and Kitces found that a rising equities portfolio beats a decreasing equities portfolio (having fewer and fewer stocks over time) and static allocation (no change to your stock/bond split throughout retirement) across most withdrawal rates and retirement horizons.

If your portfolio gets scuffed up by poor market performance early in retirement AND you gradually decrease your stock allocation, your portfolio wouldn’t hold enough stocks to capitalize on future good market returns, keeping your portfolio smaller.

Pfau and Kitces concluded that, based on historical returns, the optimal retirement glide path that provides the highest sustainable withdrawal rates is one that "begins at 30% in equities and rises to 70% in equities by the end," using a 4% withdrawal rate and a 30-year retirement horizon.

The longer the retirement horizon and the higher the withdrawal rate, the bigger the stock allocation you’ll need throughout retirement. Even so, the rising equities glide path still yielded a higher chance of success than fixed or decreasing equities allocations.

Overall, they concluded that rising equities > static allocation > decreasing equities, when it comes to decreasing the risk of running out of money. The rising equities strategy provides enough upside to sustain your portfolio while protecting you from significant downside from market crashes early in retirement.

However, their research shows that this portfolio only outperformed a handful of other static stock/bond allocations by less than a percent or two. Is this small of an advantage worth all the hoopla instead of just keeping the same asset allocation over time? I’ll leave that up to you to decide.

TL;DR - Stonks start lower, then go up. Bonds start higher, then go down. Do what you want.

Call to Action

If you’re down for some light toilet reading, check out the research by Pfau and Kitces on the rising equities portfolio. Do you think the extra effort is worth the potential for better results, or is it just adding complexity with minimal reward? Reply to this email or hit us up on Instagram to let us know!

What We’re Reading/Listening To:

ChooseFI Episode #35: Sequence of Return Risk. If you want to get more into the weeds of sequence of return risk, give it a listen. They say it’s called sequence of return risk, I say returns, I’ll let you choose what side you’re on.

Debrief on Deck

Next week, Wilson will finally break the silence on why he bought a gold bar! I’m not saying he’s a pirate, but I am saying that he hasn’t stopped referring to me as “matey” since he bought it…

As always, please reach out to us with any questions or comments you have. You can reply directly to this email or find us on social media (X (formerly Twitter) and Instagram).

Until then, stay the course.

Mike