- Dollar Debrief

- Posts

- What is My Risk Tolerance?

Figuring out your risk tolerance is like knowing how many Yankee Candles is too many: it’s hard to describe, but you’ll know when you see it.

What is my risk tolerance?

What a wonderful time to be talking about risk tolerance, when the sky of the stock market is seemingly falling thanks to a massive tech sell-off, a less than stellar US jobs report, and Japan riding the struggle bus.

Here’s my live reaction to the stock market drama:

Whatever you do, don’t go full Leeroy Jenkins and sell all of your stocks. Just ride the wave and continue to dollar cost average your money into whatever your investment of choice is (as long as it isn’t stupid). We like index funds and ETFs.

Market crashes = buying opportunities

Before talking about how to identify your risk tolerance, bear with me as I first go on a rant about risk tolerance so you know my stance.

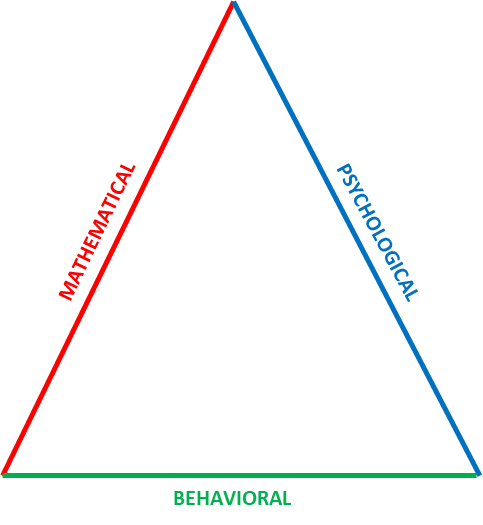

I think all financial decisions have a mathematical, behavioral, and psychological component to them, making a neat little triangle like this:

Sorry, I really didn’t feel like free-handing the word “psychological” on Microsoft Paint today

The mathematical side looks solely at numbers and probability, based on what has happened in the past and what is likely to happen in the future. For example, X decision is the most financially optimal, and therefore, is the right decision.

The behavioral side looks at the decisions and habits you are most likely to keep up with. What’s easier to keep up with, buying index funds the first of every month or spending hours each day in front of your nine-monitor work from home setup day-trading stocks?

If your setup looks like this, it’s time for an intervention

The psychological side addresses your ability to sleep at night without the persistent fear of financial ruin driving you to make rash, unsound financial decisions. This is known as your risk tolerance.

Your risk tolerance should influence a lot of your personal finance decisions, like the size of your emergency fund, how you invest your money, and how much money you should aim to accumulate in the first place.

But I have a bit of a contrarian view on risk tolerance.

I have an extremely high risk tolerance with an almost blinding faith in the stock market to increase in value long term. Because of this, I think making financial decisions through a mathematical and behavioral lens first, and weighing your risk tolerance second, is most effective.

Let me elaborate.

I think risk tolerance can be developed by continually buying into the stock market and letting compound interest and results build your confidence in this strategy. The more exposure I’ve had to the stock market and the more my money has grown, the more my confidence in the market has grown.

Investment strategies that consider only your psychological comfort are generally too risk-averse, prioritizing loss-avoidance over gains. You might feel better keeping all your money in a savings account to eliminate volatility (one risk), but you’ll also diminish your money’s value through inflation and you won’t have the assistance of compound interest with multiplying your money (two risks).

However, I’m not negating the importance of considering your risk tolerance. The best financial decision on paper will not yield your desired outcome if your inability to handle that decision mentally leads you to make poor decisions (AKA risk tolerance).

A plan you follow is far superior to a plan you ditch when the market tanks.

Find a strategy and asset allocation that balances math and mind. Understand your risk tolerance to ensure you will continue to follow the plan regardless of market conditions.

Rant complete, you made it!

So, I can’t exactly define your risk tolerance for you since it’s a personal feeling, but here are a few principles to go by to help you evaluate your own:

1) Evaluate how you feel about your investments during stock market volatility and general Wall Street pessimism (like we’re experiencing right now).

If you’re invested in the stock market, how have you felt about the decline of your stock value over the past month or so?

It’s normally best to ignore short-term stock performance to prevent yourself from doing something stupid but for this exercise, look your losses in the face.

Are you panicking in the face of all the red numbers and considering selling it all in fear that the market may continue to drop? You may need to lower your volatility.

Do you look at it and say, “meh, no big deal?” Your asset allocation is either a) right where it needs to be or b) too conservative.

2) Changing your asset allocation by adding or removing bonds is your lever for reducing or increasing volatility (and adjusting for your risk tolerance)

Stocks and bonds are the two primary investment choices to build your investment portfolio (notice I didn’t say Bitcoin).

Stocks should make up the core of your portfolio, serving as your primary wealth-builder. Bonds serve as a more stable and conservative investment option.

As a mental exercise to figure out where your asset allocation should be, start with a 100% stock allocation and work your way down to account for your risk tolerance and retirement needs.

Do you have a high risk tolerance and need aggressive investment growth to reach your retirement goals? Stick with 100% stocks.

Do you have a weak stomach for market volatility and can afford a more gradual growth trajectory to meet your retirement goals? Maybe introduce some bonds to your portfolio.

On a related note…

3) Consider your financial goals in relation to your risk tolerance, and decide which is more important to you if they are in contradiction with one another

Do you have $0 invested, want to retire in 10 years, but are afraid of investing in stocks (and real estate)? Then you’re probably out of luck. Your ambitions and your risk tolerance and competing with one another, and something needs to give.

Unless you’re into bank robbery or you have a sweet trust fund that’s about to hit.

A realistic goal for retirement over a longer time frame is better than an unrealistic, lightning fast retirement plan. Don’t be afraid to dream big, but don’t forget to be realistic.

Ensure the growth trajectory of your investment portfolio makes sense with your target timeline to retirement.

4) The further from retirement you are, the more risk you should be willing to take on (if necessary to reach your financial goals)

Notice I didn’t say “the younger you are, the more risk you should take on.”

If you’re far from your target retirement date, a few stock market crashes probably won’t kill your investments long-term.

Schwab offers a simple seven question quiz in an attempt to define your risk tolerance. However, their recommended asset allocation even for the “Moderate Allocation” is very conservative. Use this quiz to provide some insight to your risk tolerance, but it is not definitive.

All that to say, your risk tolerance is a personal, important aspect to consider when choosing your asset allocation, but it is not the only thing worth considering when setting your financial goals.

“Scared money don’t make money.” - Billy Napier, Florida Gators Head Football Coach (please give us a winning football season and don’t get fired this year)

P.S. If the University of Florida was a country, it would’ve placed 19th in overall Olympic medal count and 16th in gold medal count. No, I’m not counting Katie Ledecky’s medals.

Go Gators. Go America. Better luck in 2028, China.

Call to Action

Evaluate your current asset allocation and decide if it a) is on track to meet your retirement goals and b) meets your risk tolerance. If so, great! If not, tweak your stock/bond allocation!

What We’re Reading/Listening To:

Suits on Netflix. I know, I’m way behind on this one.

I aspire to have the brain of Mike Ross and the confidence of Harvey Specter, minus all the baggage they come with. That’d be cool.

Debrief on Deck

Next week, Wilson will talk about why we always say “stay the course.” It’s not just because it’s a catchy buzz-phrase that the people love.

As always, please reach out to us with any questions or comments you have. You can reply directly to this email or find us on social media (X (formerly Twitter) and Instagram).

Until then, stay the course.

Mike