- Dollar Debrief

- Posts

- How Should I Save for Children's College Expenses?

How Should I Save for Children's College Expenses?

The Second Most Expensive Child Cost

Mike Moricz

February 29, 2024

Some say college is the most costly child-related expense. They couldn’t be more wrong. The real answer is fruit. Every time I blink, we’re buying another carton of strawberries/blueberries for the little booger (whom I love). If you elect me as President, I promise to roll out a tax-advantaged fruit savings account.

How should I save for children’s college expenses?

College ain’t cheap, and I don’t see it getting any better in the foreseeable future.

Everything revolving around school is continuing to creep (or jump) up in price over time - tuition, fees, housing, food, transportation, and of course, those dreaded fraternity/sorority dues if you’re into that.

If you’re trying to slide down stairs, folding tables > mattresses

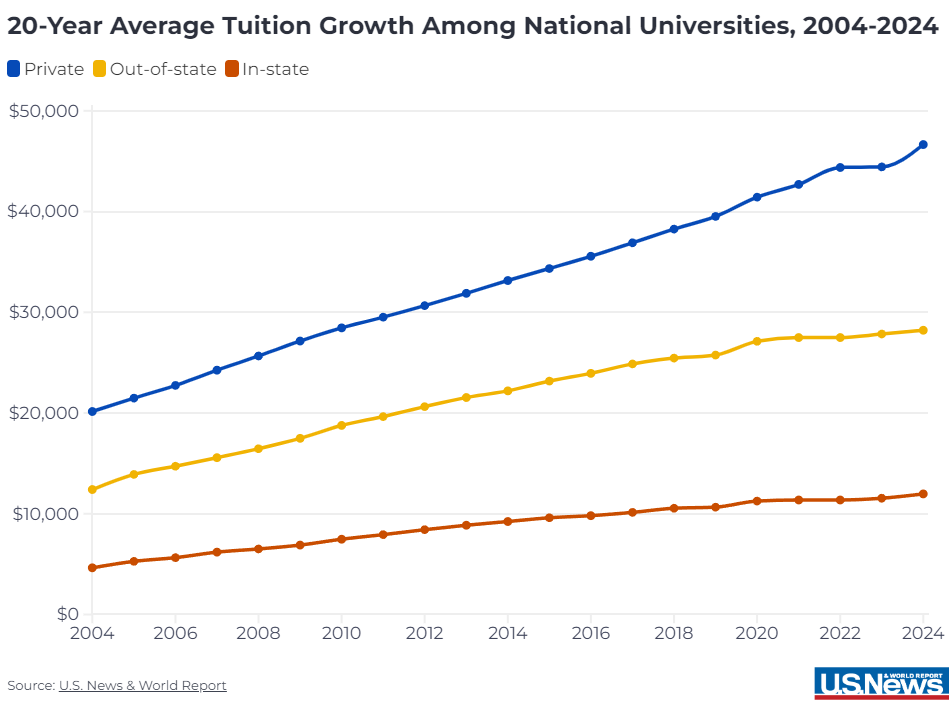

Just in the past 20 years, tuition/fees have grown 56% for in-state public university students, 38% for out-of-state public university students, and 40% for private university students, AFTER accounting for inflation.

If you decide you want to help cover some or all of your kid(s)’ college, there are a few ways you can skin the cat.

Invest money within a 529 College Savings Plan

Contribute to a 529 Prepaid Tuition Plan

Pull money from your own taxable brokerage account

Pay from your checking account throughout your child’s time in college

Let’s weigh the pros and cons of each.

529 College Savings Plan

This is my favorite option for college savings for a number of reasons.

529 College Savings Plans (normally just called the 529 plan) are tax-advantaged investment accounts specifically designed for, you guessed it… education savings for a named beneficiary. Anyone can open a 529 plan for anyone else.

A 529 plan acts like a Roth IRA, where your contributions are made after-tax but all growth and withdrawals (for qualified education-related expenses) are completely tax-free. Some states offer state tax deductions for all or a portion of 529 plan contributions, making it a good way to lower your taxable income if you’re subject to state income taxes.

Each state offers their own investment options within the 529 plan, but most offer low-fee index funds, bond funds, and other great investment options where you can let your money grow.

Money in a 529 plan can be spent on a number of things, including tuition, fees, books, school supplies, special needs expenses, and other related college expenses. It can also be used to cover up to $10,000 per year in tuition expenses for private and religious K-12 schools, plus $10,000 in existing student loan payments for the beneficiary and each of their siblings. It can be used to cover trade school/apprenticeship costs for those that opt to go that route instead of college.

If spent on nonqualified expenses, your 529 gains (not contributions) are subject to federal income tax and a 10% penalty.

You can change the 529 plan beneficiary to another family member (immediate or not) without taxes or penalties. Any leftover 529 money after the beneficiary goes to college can get rolled over to another beneficiary. Or, as of 2024, you can roll up to $35,000 of unspent 529 money into the beneficiary’s Roth IRA, giving them a nice head start toward retirement.

You can also get a jump start on saving for any future kids by opening a 529 with yourself as the beneficiary then changing it to your kids once they have a social security number. The risk with this plan is if you do not end up having kids, you will suffer the 10% penalty when rolling it over to another account or cashing out the account.

529 plans don’t have annual contribution limits but to avoid the gift tax, contributions can’t exceed more than $18,000 per person, or $36,000 per married couple.

Total account balance limits vary by state, ranging from $235,000 to $567,500. For the love of God, don’t contribute $500k+ to a 529 plan.

529 plans count as the parents’ assets, potentially impacting the beneficiary’s eligibility for federal financial aid. The pro gamer move is to have the beneficiary’s grandparents own the 529 plan, since grandparent-owned 529 plans don’t impact financial aid eligibility.

While most things remain equal, 529 plans vary slightly by state. Saving for College is a great resource to see the details of your state’s 529 plan.

It’d be political suicide for any politician that tries to degrade 529 plans in the future, so I think 529 plans are a safe place to save for college expenses.

529 Prepaid Tuition Plan

Odds are, you probably don’t have access to this plan. Only nine states offer prepaid tuition plans that are open to new enrollment: Florida, Maryland, Massachusetts, Michigan, Mississippi, Nevada, Pennsylvania, Texas, and Washington.

If you’re a resident of any state other than these nine, spare yourself the 60 seconds and skip to the next savings option.

529 Prepaid Tuition Plans allow family members to pay for a student’s college tuition at current rates, even if the child won’t attend college for several years. If college costs a nickel the day you start contributing to a prepaid tuition plan and a dollar when the beneficiary starts college, you’re only responsible for paying a nickel.

Under this plan, you either make regular payments to your state’s plan or pay it all in one lump sum during the child’s pre-college years.

But here’s the catch: prepaid tuition plans are designed to be used for tuition at any of the sponsoring state’s eligible colleges or universities. If the beneficiary wants to go to school in another state, you don’t get the benefits of cheaper tuition, you just get your money back (without gains).

Some states allow you to apply this money to out-of-state colleges/universities, but there’s often an accompanying penalty involved.

Like the 529 Savings Plan, you can transfer prepaid tuition plan funds to another family member without penalty.

Unlike 529 Savings Plans, most prepaid tuition plans don’t count non-tuition related expenses like room and board as qualified expenses.

You should only consider a 529 Prepaid Tuition Plan if a) you are certain that your child will attend an eligible in-state school, and b) you believe that the cost of college will increase at a rate greater than the stock market will grow.

I personally think the 529 College Savings Plan is a better option because I think market returns will exceed the rising cost of college, and I could see Levi going rogue and joining the circus or something weird.

Pull money from your own taxable brokerage account

This is probably my second favorite option to save for a kid’s college expenses.

Although you don’t get any tax bennies, you gain the flexibility to do whatever you want with this money without stipulations while reaping the gains of the stock market.

With this option, you don’t have to worry about your child deciding not to go to college since it’s your money and you’re free to do whatever you want with it. If Levi joins the circus, no harm, no foul.

Pay from your checking account throughout your child’s time in college

If you have a sizable income when your kid(s) are attending college, you could always just pay for it out of your income.

The perk of this option is that it allows you to maximize your own retirement contributions throughout your kid’s childhood.

However, this option doesn’t take advantage of tax-free investment growth for education. You’re paying for 100% of education expenses out of pocket, instead of letting the market double or triple your education savings.

Here’s what I plan on doing.

Em and I want to help cover college/trade school for our kids.

Our plan is to invest within a 529 College Savings Plan for each kid. If the 529 plan money dries up, we plan to cover the remainder using our monthly income first or taxable brokerage account second. Any excess 529 money will be rolled over into their Roth IRA.

Disclaimer: Ensure you’re on track for your own retirement before worrying about college savings for your children. This may seem selfish on the surface, but failing to prepare yourself for retirement and forcing your kids to fund your retirement while they have a family of their own to tend to is even more lame.

“Put your oxygen mask on first before helping others around you.” - Genghis Khan

Call to Action

Do you want to save for someone else’s college expenses? Check out the 529 plan options for each state here.

What We’re Reading/Listening To:

Freakonomics: What Exactly is College For? This is part 1 of a 4-part series all about college. The good, the bad, and the debt.

Debrief on Deck

Next week is our next Monthly Market Debrief! A lot has changed since last month, and everyone learned the value of double checking your numbers, especially Lyft.

As always, please reach out to us with any questions or comments you have. You can reply directly to this email or find us on social media (X (formerly Twitter) and Instagram).

Until then, stay the course.

Mike